@Setanta,

We're discussing the price spread between diesel and gasoline to decide whether the shift to ultra low sulfur diesel (as mandated by American and many European governments) explains the price inversion (i.e. diesel going from less expensive than gasoline to more expensive).

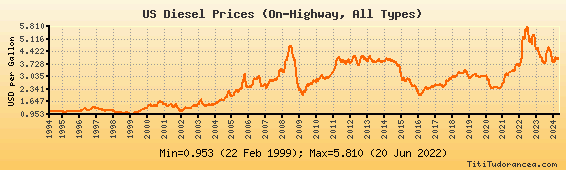

In 1994 the price of diesel was roughly a dollar a gallon while that of gasoline was about $1.15 (these are all U.S. averages). In 2002 diesel was still about a dollar and gasoline averaged $1.35. By November 2007 the average price of diesel was $3.30 and that of gasoline $3.01.

From this we note three things:

(1) Diesel became more expensive than gasoline only after the EPA mandated switch to more expensive ultra low sulfur diesel.

(2) The price differential is 29 cents, which is less than the 50 cent maximum estimated by the EPA prior to the mandated switch.

(3) Both diesel and gasoline have undergone dramatic price inflation.

The price inversion of diesel and gasoline is indeed consistent with the switch to ultra low sulfur diesel, since the price spread between diesel and gasoline is within the predicted range.

Diesel's absolute price had increased by more than 50 cents but that is irrelevant because so had the price of gasoline; and 50 cents is the predicted maximum spread between the two at the time of the mandated switch, not a limit on general price appreciation.

The explanation for the inflation and price volatility of petroleum products (be they diesel or gasoline) is clearly speculation on oil futures, in my opinion; but that is another discussion altogether.

The recent (2015) re-inversion (or parity) of diesel and gasoline prices was the subject of the original question (and my initial answer). The suggestion that diesel prices reflect what the market will bear is reasonable; the question is what factors account for the recent shift: a decrease in domestic demand in the trucking industry, an increase in domestic diesel production, or both.

{kind=link}

{kind=link}